Thursday, December 24, 2009

Monday, September 28, 2009

Branding Emerging Bioscience Companies to Attract Investors

Sasha Strauss, Managing Director at Innovation Protocol, gave a very interesting presentation at the SoCalBio Investor Conference in Santa Monica. He argues that even start-ups need to consider a branding strategy right from the start. Given the limited capital, does it make sense for a start-up to spend money on branding? Would VCs interested in investing even care about a company's brand?

To be honest, branding usually does not come to mind when evaluating an investment opportunity. Management, business model, technology, etc. are probably more important. While I don't argue that branding is important, especially as a technology gets closer to market, if there are issues with any of the other criteria, branding becomes irrelevant.

To be honest, branding usually does not come to mind when evaluating an investment opportunity. Management, business model, technology, etc. are probably more important. While I don't argue that branding is important, especially as a technology gets closer to market, if there are issues with any of the other criteria, branding becomes irrelevant.

Monday, September 21, 2009

Investing in People, Not Products

It's a cliche that "VCs invest in people first and foremost." VCs will argue that the an experienced management team knows what it takes to commercialize a technology. But does it make sense to invest in entrepreneurs with out a technology or product? Apparently, VCs think so.

Clovis Oncology raised $145 million earlier this year without a single product to commercialize. Clovis' management team consists of former executives from Pharmion, which was acquired by Celgene in 2008 for$2.9 billion . Clovis plans to acquire or license and develop oncology products. Investors include Domain Associates, New Enterprise Associates (NEA), Versant Ventures, Aberdare Ventures, Abingworth, Frazier Healthcare Ventures, and ProQuest Investments. ProjeX Therapeutics, which is backed by Sofinova, Ascalon, and Kineta are also pursuing similar acquisition/licensing models.

Given the risks and costs of developing drugs, investing in companies pursuing acquisition/licensing makes sense. Why invest in five separate companies with five seperate products and five management teams, when you can get a portfolio of products all managed by one, experienced management team. Investors still get a say in what products/technologies to license/acquire as long as they have board representation. It's simply much more efficient and cost-effective.

I think we'll start to see more and more companies like Clovis get funded in the future. It will be interesting to see how successful these companies become. Unfortunately, if this trend continues, the individual entrepreneur will have an even harder time raising capital.

Clovis Oncology raised $145 million earlier this year without a single product to commercialize. Clovis' management team consists of former executives from Pharmion, which was acquired by Celgene in 2008 for

Given the risks and costs of developing drugs, investing in companies pursuing acquisition/licensing makes sense. Why invest in five separate companies with five seperate products and five management teams, when you can get a portfolio of products all managed by one, experienced management team. Investors still get a say in what products/technologies to license/acquire as long as they have board representation. It's simply much more efficient and cost-effective.

I think we'll start to see more and more companies like Clovis get funded in the future. It will be interesting to see how successful these companies become. Unfortunately, if this trend continues, the individual entrepreneur will have an even harder time raising capital.

Wednesday, September 16, 2009

Next-Gen Genome Sequencing Attracting Investors

Despite the financial conditions, companies developing next-generation genome sequencing technology have been able to raise significant amounts of money. In August, Complete Genomics raised $45 million while Pacific Biosciences raised $68 million. Don't forget that Pacific Biosciences just raised $120 million in 2008. Both companies are pursuing the "holy grail" of genome sequencing, being able to sequence an entire human genome for less than $5,000. Keep in mind that the first human genome (Human Genome Project) took 13 years and $3 billion to sequence. See the recent article in Forbes for more on Pacific Biosciences.

While some people argue that sequencing the entire genome is not necessary, especially since 90% of the genome contains "junk" DNA, for less than $5,000, it doesn't really matter. The initial customers for genome sequencing technology will likely be drug companies for use in clinical trials, but as costs decrease, consumers will eventually become the customer. Look at the success of companies like 23andMe.

A number of next-next-generation companies, pursuing complete genome sequencing for less than $1,000, are chasing the tails of Complete Genomics and Pacific Bioscienses. They include Halcyon Molecular, Genovoxx, Lucigen, Sequenom, Oxford Nanopore Technologies, ZS Genetics, Anvantome, and VisiGen.

While some people argue that sequencing the entire genome is not necessary, especially since 90% of the genome contains "junk" DNA, for less than $5,000, it doesn't really matter. The initial customers for genome sequencing technology will likely be drug companies for use in clinical trials, but as costs decrease, consumers will eventually become the customer. Look at the success of companies like 23andMe.

A number of next-next-generation companies, pursuing complete genome sequencing for less than $1,000, are chasing the tails of Complete Genomics and Pacific Bioscienses. They include Halcyon Molecular, Genovoxx, Lucigen, Sequenom, Oxford Nanopore Technologies, ZS Genetics, Anvantome, and VisiGen.

Thursday, August 27, 2009

Highlights from California Bioscience Business Roundtable

A number of topics was discussed at the recent California Bioscience Business Roundtable including the venture financing environment, follow-on biologics (biosimilars), and health care reform.

Doug Kelly, MD from Alloy Ventures gave a pretty bleak outlook on venture financing; he even used the word "Armageddon" in describing the current environment. I was actually surprised to hear that he was not looking at any biopharmaceutical drug investments at the moment. Uncertainty surrounding biosimilars regulation and the FDA approval process were making it difficult to make any big bets. Adding to that is the financial crisis that is limiting the ability of VCs to make investments. Bill Gurley from Benchmark Capital has a great explanation of how the financial environment is impacting VC on his blog. I thought I was relatively pessimistic but Doug Kelly really depressed me!

Lori Reilly from PhRMA and Sam Youngman, White House correspondent from The Hill, discussed health care reform. The Democrats have not been doing a good job advocating health care reform apparently. Although, the recent passing of Senator Ted Kennedy might be a catalyst that galvanizes the Democrats. President Obama should start making an even bigger push for reform as a result. It's difficult to see whether any legislation will get passed by the end of the year given the amount of time Congress has left, but eventually, a compromised bill that doesn't make anyone happy will get signed. If the Democrats cannot get something signed soon though, the opportunity for health care reform will eventually die, similarly to what occurred during the Clinton administration.

Geoff Eich, Director of Regulatory Affairs at Amgen, highlighted the success of follow-on biologics regulation in the EU. For example, interferon biosimilars had different characteristics than branded interferon and caused relapses in patients. Ultimately, the EU rejected the interferon biosimilars. Human growth hormone (hGH) biosimilars suffered problems with side effects initially until it was discovered that there were problems with the purification process. Once the problem was solved, EU regulators approved hGH biosimilars. These examples clearly show that there will be a number of technical hurdles for biosimilar manufacturers to overcome. Just imagine how difficult it will be to manufacture antibodies if it's this difficult to do more simple proteins.

Doug Kelly, MD from Alloy Ventures gave a pretty bleak outlook on venture financing; he even used the word "Armageddon" in describing the current environment. I was actually surprised to hear that he was not looking at any biopharmaceutical drug investments at the moment. Uncertainty surrounding biosimilars regulation and the FDA approval process were making it difficult to make any big bets. Adding to that is the financial crisis that is limiting the ability of VCs to make investments. Bill Gurley from Benchmark Capital has a great explanation of how the financial environment is impacting VC on his blog. I thought I was relatively pessimistic but Doug Kelly really depressed me!

Lori Reilly from PhRMA and Sam Youngman, White House correspondent from The Hill, discussed health care reform. The Democrats have not been doing a good job advocating health care reform apparently. Although, the recent passing of Senator Ted Kennedy might be a catalyst that galvanizes the Democrats. President Obama should start making an even bigger push for reform as a result. It's difficult to see whether any legislation will get passed by the end of the year given the amount of time Congress has left, but eventually, a compromised bill that doesn't make anyone happy will get signed. If the Democrats cannot get something signed soon though, the opportunity for health care reform will eventually die, similarly to what occurred during the Clinton administration.

Geoff Eich, Director of Regulatory Affairs at Amgen, highlighted the success of follow-on biologics regulation in the EU. For example, interferon biosimilars had different characteristics than branded interferon and caused relapses in patients. Ultimately, the EU rejected the interferon biosimilars. Human growth hormone (hGH) biosimilars suffered problems with side effects initially until it was discovered that there were problems with the purification process. Once the problem was solved, EU regulators approved hGH biosimilars. These examples clearly show that there will be a number of technical hurdles for biosimilar manufacturers to overcome. Just imagine how difficult it will be to manufacture antibodies if it's this difficult to do more simple proteins.

Wednesday, August 19, 2009

AARP Got Follow-on Biologics Analysis Wrong

As the health care reform debate rages, I have been been looking at the potential impact of follow-on biologics (or biosimilars) on the drug industry. I came across an article from the AARP Rx Watchdog Report (May 2009) that made an argument in favor of follow-on biologics regulation. Granted, the AARP is not necessarily impartial, but the analysis from the AARP's Public Policy Institute is a bit misleading.

The AARP compares the treatment costs for small-molecule drugs and biologics and argues that biologics are too costly when used to treat the same condition, such as rheumatoid arthritis or multiple sclerosis. This argument can be misleading because the AARP does not compare the efficacy and safety of small-molecule drugs vs. biologics. It's like comparing an old Pinto to a brand new Mercedes Benz and saying that the Mercedes is too expensive. Of course, people are willing to pay more for the Mercedes because there is more value in such a car, as should insurers for better treatments.

The AARP also argues that sales of the top selling biologics more than cover the average cost of developing a biologic ($1.2 billion). First of all, the sales have to cover the development costs in addition to other costs. Otherwise, drug companies would not be in business for long. Secondly, it's unfair to cherry pick only the top selling drugs; it's not an apples-to-apples comparison.

I agree with the AARP that biologics have (to a certain extent) contributed to rising health care costs. I'm not a pricing expert, but some biologics (not all) do seem to be overpriced. It's obvious that rising health care costs are unsustainable. I also believe that follow-on biologics regulation is inevitable. Refer to the FTC findings on follow-on biologics competition for more analysis.

The AARP compares the treatment costs for small-molecule drugs and biologics and argues that biologics are too costly when used to treat the same condition, such as rheumatoid arthritis or multiple sclerosis. This argument can be misleading because the AARP does not compare the efficacy and safety of small-molecule drugs vs. biologics. It's like comparing an old Pinto to a brand new Mercedes Benz and saying that the Mercedes is too expensive. Of course, people are willing to pay more for the Mercedes because there is more value in such a car, as should insurers for better treatments.

The AARP also argues that sales of the top selling biologics more than cover the average cost of developing a biologic ($1.2 billion). First of all, the sales have to cover the development costs in addition to other costs. Otherwise, drug companies would not be in business for long. Secondly, it's unfair to cherry pick only the top selling drugs; it's not an apples-to-apples comparison.

I agree with the AARP that biologics have (to a certain extent) contributed to rising health care costs. I'm not a pricing expert, but some biologics (not all) do seem to be overpriced. It's obvious that rising health care costs are unsustainable. I also believe that follow-on biologics regulation is inevitable. Refer to the FTC findings on follow-on biologics competition for more analysis.

Wednesday, August 12, 2009

Top Life Science VCs

FierceBiotech just released a list of "top" life science VC firms. The article includes descriptions and different deals of each firm. It's a good resource to learn more about the life science VC firms listed, in particular what types of therapeutic areas and at what stage of development they are focused on. The definition of "top" here can be a bit misleading though. I believe that the term "top" used in the article really means most active. Nonetheless, all of the firms listed have a very good track record of making investments. There are many more VC firms that invest in life sciences, so entrepreneurs looking for financing shouldn't limit themselves to this list only.

Tuesday, August 4, 2009

Deathwatch update

La Jolla Pharmaceuticals recently announced its plans to liquidate assets. Its lupus drug Riquent failed to show efficacy in Phase III studies in February, and the company failed to find any additional financing.

TorreyPines Therapeutics will be shutting its doors and liquidating its assets, which include ionotropic glutamate receptor antagonist, tezampanel. The FDA had approved a Phase III study for tezampanel in acute migraine but required a QT/QTc study in parallel with the first Phase III pivotal trial. Unfortunately, TorreyPines was unable to secure a partner to help develop tezampanel before running out of money.

DiObex, which had a low-dose glucagon for diabetes entering Phase II, was also forced to shut down and sell its assets after investors decided that the valuation from new investors was too low.

Other life science companies that have struggled to find financing include: Nanogen, Isolagen, Oscient Pharmaceuticals, Luna Innovations, Biopure, and Epix Pharmaceuticals. Check out the WSJ's "Turning Out the Lights" series of posts for other venture-backed company shutdowns.

TorreyPines Therapeutics will be shutting its doors and liquidating its assets, which include ionotropic glutamate receptor antagonist, tezampanel. The FDA had approved a Phase III study for tezampanel in acute migraine but required a QT/QTc study in parallel with the first Phase III pivotal trial. Unfortunately, TorreyPines was unable to secure a partner to help develop tezampanel before running out of money.

DiObex, which had a low-dose glucagon for diabetes entering Phase II, was also forced to shut down and sell its assets after investors decided that the valuation from new investors was too low.

Other life science companies that have struggled to find financing include: Nanogen, Isolagen, Oscient Pharmaceuticals, Luna Innovations, Biopure, and Epix Pharmaceuticals. Check out the WSJ's "Turning Out the Lights" series of posts for other venture-backed company shutdowns.

Wednesday, July 29, 2009

VC Career Advice

I've been talking recently to a number of people interested in pursuing a career in VC. It's really difficult to offer any good advice as to the best way to become a VC because there are a number of different paths to choose from. VCs can come from investment banking, management consulting, start-ups, big corporations, etc. There is no "typical" career track to follow to break into VC.

With a very limited number of openings each year and many qualified applicants, VC firms can be very picky in their hiring; most VCs working in life sciences have either an M.D. or Ph.D., and several have an M.B.A. in addition to the other degrees. As the VC industry contracts (see figure below, source: WSJ), there will be even fewer positions available.

While there's no guarantee of landing a job, I believe the Kauffman Fellows Program is a good way to get your foot in the door. Search firms, such as Glocap, Pinnacle Group, and Polachi, might also be helpful.

I'd like clarify a misconception that some people might have about being a VC. I absolutely love my job, and I'm very fortunate to work with very smart, stimulating people. It's a lot of fun meeting entrepreneurs with really interesting ideas about solving the world's problems. There is no such thing as a perfect job though, as every job has its pros and cons, and being a VC is no different. Let me know if there are any jobs out there that will pay you to sleep with models (j/k). While it may appear that being a VC can be somewhat glamorous and lucrative, it is definitely not always the case; especially if you're not a partner. I rent a one-bedroom apartment and lease my car. I have about $35K remaining of almost $100K in student loans to pay off. I am by no means poor, but my life is not very extravagant either. I believe most VCs who aren't partners live relatively modest lifestyles.

Even if you overcome the odds and land a position, the probability of becoming a partner is relatively low. With fewer firms remaining, there are even fewer partner positions available. Ultimately, "you eat what you kill" in this business, and if my investment decisions result in poor returns, I won't survive in this business for too long.

Check out John Gannon's VC Career Resource page for more information.

With a very limited number of openings each year and many qualified applicants, VC firms can be very picky in their hiring; most VCs working in life sciences have either an M.D. or Ph.D., and several have an M.B.A. in addition to the other degrees. As the VC industry contracts (see figure below, source: WSJ), there will be even fewer positions available.

While there's no guarantee of landing a job, I believe the Kauffman Fellows Program is a good way to get your foot in the door. Search firms, such as Glocap, Pinnacle Group, and Polachi, might also be helpful.

I'd like clarify a misconception that some people might have about being a VC. I absolutely love my job, and I'm very fortunate to work with very smart, stimulating people. It's a lot of fun meeting entrepreneurs with really interesting ideas about solving the world's problems. There is no such thing as a perfect job though, as every job has its pros and cons, and being a VC is no different. Let me know if there are any jobs out there that will pay you to sleep with models (j/k). While it may appear that being a VC can be somewhat glamorous and lucrative, it is definitely not always the case; especially if you're not a partner. I rent a one-bedroom apartment and lease my car. I have about $35K remaining of almost $100K in student loans to pay off. I am by no means poor, but my life is not very extravagant either. I believe most VCs who aren't partners live relatively modest lifestyles.

Even if you overcome the odds and land a position, the probability of becoming a partner is relatively low. With fewer firms remaining, there are even fewer partner positions available. Ultimately, "you eat what you kill" in this business, and if my investment decisions result in poor returns, I won't survive in this business for too long.

Check out John Gannon's VC Career Resource page for more information.

Thursday, July 23, 2009

BioPharma Acquisition Spree Continues

Bristol-Myers Squibb recently announced its acquisition of Medarex for $2.1 billion (at $16 per share, about a 90% premium over its previous close). As I mentioned over three years ago, analysts had been speculating about Medarex's acquisition after Amgen acquired Abgenix in 2005. Why did Bristol-Myers finally pull the trigger after all this time? I suspect that after Bristol-Myers was outbid by Lilly for control of ImClone, BMS wanted to reinforce its biologics franchise. That and the fact that Medarex shares have taken a beating since August of last year. Bristol-Myers and others have been signaling that they would take advantage of low valuations to make acquisitions. I believe that this buying spree will continue for the near-term as the fundamentals haven't changed yet: relatively low valuations and cash-rich buyers facing generic competition and limited R&D productivity.

Monday, July 20, 2009

Dow Jones VentureSource 2Q09 Results

Dow Jones VentureSource released results for U.S. VC Financing for Q2. VC financing during Q2 rebounded 32% from a dismal Q1 but was down 37% compared to the same quarter last year. For the first time, more capital flowed into health care than IT companies. While biopharmaceutical and medical device investments decreased, the health care services sector had a great quarter, improving nearly three-fold.

This rotation to health care is pretty amazing considering the capital requirements and risks associated with health care startups relative to IT companies. I believe that investors recognize that there are still healthy exit opportunities in health care compared to other industries. In my opinion, there is still a lot of downward pressure on the VC industry. Hopefully, health care can remain a silver lining moving forward.

“Health care investment was the only sector to spring back to levels seen before the economic meltdown that began in the third quarter of 2008."The following figure summarizes the proportion of dollars invested into the different industries (click on figure for larger view).

This rotation to health care is pretty amazing considering the capital requirements and risks associated with health care startups relative to IT companies. I believe that investors recognize that there are still healthy exit opportunities in health care compared to other industries. In my opinion, there is still a lot of downward pressure on the VC industry. Hopefully, health care can remain a silver lining moving forward.

Friday, July 17, 2009

Signs of Life in Life Sciences VC

After a rough 1st quarter, the recently released OnBioVC 2Q09 Trends Analysis shows that life sciences VC funding increased year-over-year by 31%, totaling about $1.71B for 2Q09 vs. $1.18B for 2Q08. Funding for the quarter increased about 20% relative to Q1, which was approximately $1.43B. Not surprisingly, most of the money (almost $1B) went to later-stage companies (Series C and beyond).

It will be interesting to see what the NVCA/VentureSource Q2 results will be. I'm wondering if VC firms are rotating into life sciences deals or whether other industries will see a healthy increase in VC funding. I can see why VCs are interested in life sciences investments at the moment given the exit opportunities. I am a bit surprised, though, by the magnitude of the increase in life sciences funding compared to last year. Maybe LPs are loosening up faster than I expected, which is great for start-ups seeking capital.

It will be interesting to see what the NVCA/VentureSource Q2 results will be. I'm wondering if VC firms are rotating into life sciences deals or whether other industries will see a healthy increase in VC funding. I can see why VCs are interested in life sciences investments at the moment given the exit opportunities. I am a bit surprised, though, by the magnitude of the increase in life sciences funding compared to last year. Maybe LPs are loosening up faster than I expected, which is great for start-ups seeking capital.

Tuesday, June 30, 2009

A Case for Preclinical Biopharma Companies

Despite the talk about how later-stage companies are being more favored, Jeff Himawan from Essex Woodlands Health Ventures made a very good case for preclinical stage biopharmaceutical investments at the recent LARTA Life Sciences Venture Forum. Concert Pharmaceuticals recently announced a partnership with GSK for three preclinical programs potentially worth over $1 billion in milestone and option payments. The lead compound, CTP-518, is a novel HIV protease inhibitor expected to enter Phase I trials the second half of 2009. Chroma Therapeutics also entered into a partnership with GSK for four discovery and development programs to identify small molecule therapeutics, including a macrophage-targeted HDAC inhibitor program for inflammatory disorders such as rheumatoid arthritis. The partnership is also potentially worth more than $1 billion. Last year, Daiichi Sankyo acquired U3 Pharma AG for $235 million. U3's lead program, which is partnered with Amgen, is a fully-human HER-3 monoclonal antibody that will start clinical trials by the end of the year. Obviously, investing in preclinical programs are risky, but with most investors focusing on later-stage opportunities, there might be some good bargains at the early-stage.

Thursday, June 25, 2009

Global Trends in VC 2009

The Deloitte 2009 Global Venture Capital Survey results suggest that, not surprisingly, the majority of firms plan to maintain or decrease their level of investment in the future. The pie chart below shows the proportion of U.S. firms that intend to change their level of investments in terms of capital and number of companies. There's also a shift towards later-stage companies (figure not shown).

There is a silver lining though. The medical device group appears to be favored by global VC firms compared to other sectors.

There is a silver lining though. The medical device group appears to be favored by global VC firms compared to other sectors. The following pie charts show the proportion of U.S. venture firms' anticipated change in the level of investment for biopharmaceutical and medical device companies.

The following pie charts show the proportion of U.S. venture firms' anticipated change in the level of investment for biopharmaceutical and medical device companies.

There is a silver lining though. The medical device group appears to be favored by global VC firms compared to other sectors.

There is a silver lining though. The medical device group appears to be favored by global VC firms compared to other sectors. The following pie charts show the proportion of U.S. venture firms' anticipated change in the level of investment for biopharmaceutical and medical device companies.

The following pie charts show the proportion of U.S. venture firms' anticipated change in the level of investment for biopharmaceutical and medical device companies.

Sunday, June 21, 2009

Right-sizing VC

Paul Kedrowsky of the Kauffman Foundation recently published a not-so flattering article about venture capital, Right-Sizing the U.S. Venture Capital Industry. He outlines why the VC industry will likely shrink over the next few years. His argument is simple: VCs must offer investors competitive returns for the industry to be viable. Unfortunately, VC performance has been relatively poor since the dot-com bubble burst. The amount of capital committed needs to return to levels when the VC industry generated competitive returns. So how much should the industry contract by?

"...we should expect it to fall by half to a $12 billion per year investing pace from it current $25 billion (and higher) rate."The thesis is similar to Fred Wilson's Math Problem. I also believe that the VC industry will contract simply because many LPs will not have as much capital to invest. It will be interesting to see how quickly this right-sizing plays out. Unfortunately for entrepreneurs, obtaining capital from VCs will get more difficult as a result of right-sizing. Hopefully, other avenues (e.g. government grants, angel funds, friends and family, etc.) will be able to fill in some of the gap.

Tuesday, June 16, 2009

IPO Window Possibly Reopening

At the recent Wilson Sonsini Goodrich & Rosati Medical Device Conference in San Jose, Piper Jaffray investment bankers, Richard Gustafson and Neil Riley, presented data suggesting that the IPO market was possibly reopening.

As the stock markets recovered in 2003, the number of IPOs increased (see table below). The 2009 market recovery is showing a similar trend. Average revenue for IPO companies in 2003 was $165M. Similarly, average revenue for IPO companies in 2009 $149M. So far, the IPOs in 2009 have performed well, up about 35%. Due to increased volatility, a lot of money is currently on the sidelines. As volatility returns to normal, the bankers believe that some of that capital will go into IPOs.

The bankers admitted that unemployment is now much higher than it was in 2003, 9.4% vs. 6.5%, respectively. Unemployment is a lagging indicator though, so it should have less an impact on the markets' recovery. They did expect the recovery to be gradual and protracted.

The bankers admitted that unemployment is now much higher than it was in 2003, 9.4% vs. 6.5%, respectively. Unemployment is a lagging indicator though, so it should have less an impact on the markets' recovery. They did expect the recovery to be gradual and protracted.

Before everyone gets too excited, keep in mind that the companies that have done an IPO this year were profitable and growing at 20%. While some medical device companies can make that claim, most biopharmaceutical companies can't. For what it's worth, I remain a bit skeptical about a near-term recovery for a number of reasons - too many to discuss now. But, I am hopeful that the IPO market will eventually recover.

As the stock markets recovered in 2003, the number of IPOs increased (see table below). The 2009 market recovery is showing a similar trend. Average revenue for IPO companies in 2003 was $165M. Similarly, average revenue for IPO companies in 2009 $149M. So far, the IPOs in 2009 have performed well, up about 35%. Due to increased volatility, a lot of money is currently on the sidelines. As volatility returns to normal, the bankers believe that some of that capital will go into IPOs.

The bankers admitted that unemployment is now much higher than it was in 2003, 9.4% vs. 6.5%, respectively. Unemployment is a lagging indicator though, so it should have less an impact on the markets' recovery. They did expect the recovery to be gradual and protracted.

The bankers admitted that unemployment is now much higher than it was in 2003, 9.4% vs. 6.5%, respectively. Unemployment is a lagging indicator though, so it should have less an impact on the markets' recovery. They did expect the recovery to be gradual and protracted.Before everyone gets too excited, keep in mind that the companies that have done an IPO this year were profitable and growing at 20%. While some medical device companies can make that claim, most biopharmaceutical companies can't. For what it's worth, I remain a bit skeptical about a near-term recovery for a number of reasons - too many to discuss now. But, I am hopeful that the IPO market will eventually recover.

Monday, June 1, 2009

Financing for Med Device Startups in an Uncertain Economy

I attended the SVASE (Silicon Valley Assoc. of Startup Entrepreneurs) sponsored event entitled "Financing Strategies for Medical Device Startups in an Uncertain Economy" the other week. The panel consisted of Frank Rahmani from Cooley Godward Kronish, Ted Driscoll of Claremont Creek Ventures, Albert Cha of Vivo Ventures, and Michael Bates of Life Science Angels and Band of Angels. There were a lot of interesting conversations, but the discussion on different financing opportunities is important to highlight. I've listed some of them below:

- Government - SBIR grants are a great way to finance a startup without diluting equity, but the grant process can be time consuming and competitive.

- Incubators - For a stake in your startup, incubators provide lab space, administrative assistance, strategic guidance, etc. Although incubators usually don't provide direct capital, they will assist in finding angels and VCs to invest. Attending the meeting was Mike Partsch, entrepreneur and former VC, who has successfully launched a few medical device companies from his incubator. The Foundry is another medical device incubator with a number of companies that have been financed.

- Angels - Angels typically provide seed-stage financing to startups that are "too early" for most VCs. Raising money from Angel groups is like "herding cats" to paraphrase Michael Bates, but the members are usually seasoned entrepreneurs, who can provide very valuable advice to early-stage startups. Angel networks commonly work closely with VCs and can also assist in obtaining VC financing.

- Venture capital - In addition to providing cash, VCs offer strategic guidance, help recruit management, etc. When trying to raise money, "VCs are not all the same," as one panelists stated. Some firms focus on early-stage companies, while others invest in only health care IT startups. It's important to identify the right match. Also, make sure that there are no conflicts in the VC's current portfolio, i.e. companies with competitive technologies.

- Corporate investors - Corporate investors usually wait until most of the risk is removed from a startup before investing. Depending on the deal terms, a corporate investment may limit the number of potential acquirers in the future.

Wednesday, May 27, 2009

Compensation for Management at Startups

If your interested in the compensation for executives for life sciences/medical device startups, check out the 2008 Compensation and Entrepreneurship Report in Life Sciences at Altgate. The survey provides data about cash and equity compensation split by a variety of parameters (e.g. position, geography, biopharmaceutical vs. medical device company, etc.). For example, the average base salary for a CEO at a company with one or less financing round ranged from $220,000 to $325,000. Equity owned by the same CEO ranged from 4.9% to 7%. As the company raises additional rounds of financing, the CEO base salary would generally increase, but equity would become diluted. If the CEO was a founder, he/she would usually have considerably more equity in the company but a lower base salary. Total cash compensation (base and bonus) for CEOs at biopharmaceutical companies was a little better than for their counterparts at medical device companies, $410,000 vs. $371,000, but equity holdings were slightly better for medical device CEOs, 6.04% vs. 5.12%.

Wednesday, May 20, 2009

Pitching to Investors: Become a PUA

Certain rules should be followed when making a pitch to VCs. I'm a big fan of Presentation Zen for its minimalist philosophy on presentations. Jason Mendelson, of Ask the VC, recently posted some common sense advice from communications consultant Matt Eventoff about pitching to investors. Carin Canale, President of Porter Novelli Life Sciences, recently wrote a more specific article in Nature Biotechnology about how to organize your slide presentation. It's worth saying over and over again that a clear message is critical when presenting to investors. While different VCs will focus on different risks (e.g. market, management, technology, financing, etc.), if the value proposition isn't clear, these other issues won't matter. I often hear pitches that focus mostly on technology but never really address how the technology solves a problem. Pitching to investors is kind of like trying to pick up someone at a bar - someone that gets a lot of suitors. The initial few minutes are critical to make a good impression, and you better show some value. That being said, don't be too disheartened if you get rejected. As in the dating world, becoming a PUA (pick up artist) takes practice. If you have time, read The Game.

Friday, May 15, 2009

Update on PIPEs

A little while ago, I wrote a post on the attractiveness of PIPEs to some VCs due to valuations. The PIPEs Report released a first quarter review of PIPE transactions in April. Despite a decrease in the overall number of PIPE deals (35% decrease in the total number of deals completed and over 75% decrease in total value), biopharma PIPEs increased. There were 43 biopharma PIPEs out of a total of 101 in Q1. For the same quarter last year, biopharma deals only accounted for 15% of all PIPEs vs. 23% this year. Biopharma companies raised over $600M this quarter on PIPE transactions. It's hard to say whether the attraction of PIPEs will continue or whether VCs will return to more traditional private placements. There is evidence that VCs do add value to public companies that they invest in. It will be interesting to see how these biopharma PIPEs perform in the next year or so.

Friday, May 8, 2009

David and Goliath

VCs often tell entrepreneurs that they're looking for "game-changing" technology and a solid management team. It's become a cliché, but investors believe that having the right management team is even more important than the technology. A great article in The New Yorker by Malcolm Gladwell, author of Tipping Point, Blink, and Outliers, reinforces why the two investment criteria mentioned above are so important to VCs. Gladwell's article talks about how basketball teams that are smaller and have less athletic ability can beat much better teams. He also gives an example of how a small military force with fewer resources can overcome a larger army, as in the case of Lawrence of Arabia against the Turkish army. Again and again, throughout history, Davids beat Goliaths. What the Davids often have in common are two things: unrelenting effort/persistence and an unconventional strategy. For health care startups to succeed, the same can be said. Genentech and Amgen are good examples. These companies developed innovative technologies at the time, and management had the insight to recognize markets that were overlooked by Big Pharma. Management also had the dedication to overcome many years of setbacks and challenges. Becoming a successful startup is much more complicated than just working really hard and having technology, but one can see why it's necessary to start with them.

Wednesday, May 6, 2009

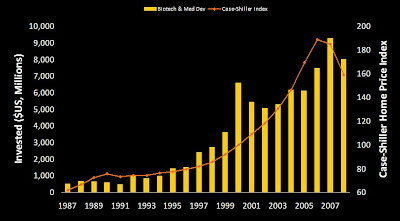

Asset Bubbles

Easy credit, in addition to other factors, contributed to the real estate bubble. I believe that venture capital also benefited from cheap money. I looked at the amount of venture capital invested in biotechnology and medical devices (from Thomson Reuters, NVCA Yearbook 2009) and compared it to the Case-Shiller Home Price Index (from Standard & Poor's). As the chart below shows, VC investments in biotechnology and medical devices (bars) have followed a similar path to that of home prices (line). While there shouldn't necessarily be any correlation between the two, the abundance of cheap money seems to have helped over inflate a number of assets. If you believe that real estate is overpriced and that the correlation to hold, VC investments still has a ways to fall.

Monday, May 4, 2009

The Entrepreneur's Guide to a Biotech Startup

Being a former scientist, I find entrepreneurs' passion and intelligence inspiring. They are part of the reason why I enjoy working in venture capital so much, and I have the utmost respect for entrepreneurs. It is extremely difficult to raise venture capital, and very few entrepreneurs/scientists are successful at it. Unfortunately, the developing a drug therapy is capital intensive. Some people, such as Johnny Stine, are developing drugs without any VC funding - he's pretty amazing, and I hope he's successful. Johnny Stine is a great example of doing research on a shoestring budget, and he exemplifies the entrepreneurial spirit. For most entrepreneurs however, raising money is a necessity. Entrepreneurs/scientists that have never had to raise before need to be prepared and understand what investors are looking for - especially now, since it will be more difficult to find capital. I usually refer people to The Entrepreneur's Guide to a Biotech Startup, Fourth Edition, by Peter Kolchinsky. It's available for download for free at Evelexa.com. Although it's a bit dated - it hasn't been updated since 2004 - it remains a great resource for scientists thinking about taking the plunge into entrepreneurship. Even to this day, I use it as a reference every once in a while.

Thursday, April 30, 2009

The Coming Contraction

As I mentioned in a previous post, I believe the VC industry will contract mainly because some funds will have a difficult time raising new money from LPs in this new financial environment. Fred Wilson has a very good post on the "Math Problem" that the VC industry has and why the asset class will likely shrink because of it. One could argue that the Math Problem doesn't apply as much to the life sciences sector since M&A activity remains relatively robust, but we'll leave that discussion for another day. While less capital is good for LPs, it does make things harder for entrepreneurs trying to raise. As the industry emerges from the current financial crisis, I believe that capital efficiency will be the focus of most VCs, both in technology and life sciences. It's not like capital efficiency wasn't important before, but it will definitely be more now. For the entrepreneur, that means doing more with less. It likely means that fewer primary care drugs and more specialty drugs get funded. Unfortunately, it also means that fewer startups in total will likely get funded.

Thursday, April 23, 2009

Deathwatch

Just to see how tough it is for biopharmaceuticals companies trying to obtain financing, I put together a list of firms that have released some negative press in the past few months. The list is by no means comprehensive, considering that private companies are not obligated to report their financing situation.

Genaera Corporation, Isolagen Inc., Torrey Pines Therapeutics, Evotec AG, La Jolla Pharmaceuticals, Trubion Pharmaceuticals, Northstar Neuroscience, Targeted Genetics, Cardiace Science, Telik, Oscient Pharmaceuticals, Advanced Life Sciences, DeCode Genetics, Anesiva, and DiObix.

Update: Sorry for any confusion. I didn't mean to imply that any of the companies listed above would go bankrupt. I was just pointing out that many companies need to conserve cash given the current financing environment.

Genaera Corporation, Isolagen Inc., Torrey Pines Therapeutics, Evotec AG, La Jolla Pharmaceuticals, Trubion Pharmaceuticals, Northstar Neuroscience, Targeted Genetics, Cardiace Science, Telik, Oscient Pharmaceuticals, Advanced Life Sciences, DeCode Genetics, Anesiva, and DiObix.

Update: Sorry for any confusion. I didn't mean to imply that any of the companies listed above would go bankrupt. I was just pointing out that many companies need to conserve cash given the current financing environment.

Monday, April 20, 2009

VentureSource Q1 Numbers Not Very Pretty

Dow Jones VentureSource just released Q1 results for VC activity in the US. Not surprisingly, the numbers weren't very pretty. Total dollars invested decreased by 50% from the same quarter last year. The one bright spot - if you can really call it that - was health care, which only declined 34%. M&A activity in health care has kept VCs interested in the space. VC investments in all the other sectors declined 50% or more. So have we hit the bottom? Are VCs going to jump back in and start deploying cash? Will companies finally be able to raise capital? Unfortunately, I think it's too early to tell. Even if we have bottomed out, I don't expect too many VCs will rush back in right away. It's probably going to be a drawn out process as investors slowly test the waters.

Thursday, April 16, 2009

Discovering Bacteria's Communication System

Bonnie Bassler, microbiologist from Princeton, recently gave a very interesting presentation at the TED2009 Conference on signaling between bacteria. The part of the her talk that really interested me was the fact that humans and many bacteria have a symbiotic relationship. Certain bacteria help us digest food for example. It's no wonder that most antibiotics have side effects since they indiscriminately target the beneficial bacteria as well as the harmful bacteria. Professor Bassler's research suggests that developing molecules that target the way bacteria communicate with each other will eventually lead to novel antibiotics. I believe that targeting intra-species bacterial signaling, as she proposes, is extremely promising. Unfortunately, antibiotics that inhibit inter-species communications might result in side effects, due to non-selectivity and negatively impact the bacteria that help humans function. Nonetheless, her presentation provides a fascinating look at how bacteria interact, and it's worth watching.

Monday, April 13, 2009

DiObex Shuts Down and Sells Assets

About a month ago, I wrote a post about potential opportunities to pick up assets from distressed companies. Last week, DiObex announced that it failed to raise additional capital and was effectively shutting down. The company was financed previously by venture firms including Domain Associates, Inventages Venture Capital, Pequot Ventures, and Sofinnova Ventures. The board has now decided to sell the company's assets, mainly diabetes drug (DIO-901) entering Phase II, to recoup invested capital. Although the diabetes market is huge, getting regulatory approval for a diabetes drug can be difficult, time-consuming, and expensive. Recent safety concerns with diabetes drugs, e.g. Avandia, has made the FDA very cautious, and long-term safety is always an issue since most diabetes drugs are taken chronically. This might be an opportunity for a large pharmaceutical company, e.g. Lilly or Novo Nordisk, to pick up an asset on the cheap. Unfortunately, I don't believe this will be the last we hear about companies having to sell their assets this year.

Tuesday, April 7, 2009

Laying Down Some PIPE

A PIPE (private investment in public entity) occurs when a private investor (e.g. a VC/PE fund) purchases shares of a publicly traded company. Recently, VCs have been showing a lot of interest in PIPEs. Sunesis just announced that the company secured $43.5M in a private placement led by Bay City Capital. Other recent PIPEs include Xenoport, ATS Medical, and Stereotaxis. The main reason VC funds are doing PIPEs is because valuations of public companies have been indiscriminately slaughtered; a number of companies are trading for less than cash. Another advantage of PIPEs is that of liquidity (theoretically), especially with the IPO window closed. VCs normally don't do many PIPE transactions. Public companies are generally left to mutual funds and hedge funds to invest in. PIPEs don't always result in a board seat for the VC; thus no active management or much control over the investment. Another reason PIPEs aren't too common is that a portion of the financing is spent on adhering to SEC regulations for public companies rather than improving the business; Sarbanes-Oxley is a common complaint. Liquidity is not always guaranteed; even though the companies are public, there might not be enough float to sell the shares. In the current financial crisis, some PIPEs make sense though. Unfortunately, PIPEs only make it more difficult for private startups looking to raise money.

Tuesday, March 31, 2009

Corporate Venture Capital

Merck KGaA recently launched a corporate venture capital fund called Merck Serono Ventures. The fund intends to invest $54 million in biotechnology startups over the next five years. Even Google's new venture arm plans to invest in biotechnology companies. It's a bit of a surprising move; most life sciences corporate venture groups have not fared well. Merck Capital Ventures, for example, was shut down last year. Fred Wilson has some great comments on the inherent conflicts of corporate venture capital arms on his blog, A VC. Nonetheless, this is good news for startups trying to raise capital in a very challenging environment.

Sunday, March 29, 2009

What Are Genetech Scientists Going To Do?

Now that the Roche acquisition of Genentech has been completed, a lot of Genentech scientists will have to decide whether to stay with Roche or not. Roche management has said that they will not do anything to change Genentech's scientist-friendly culture, but I believe that a lot will depend on what former Genentech CEO, Art Levinson, will ultimately end up doing. Art, himself a former scientist at Genentech, is much beloved by all of Genentech, not just R&D. If his role is diminished or if he leaves, many of the scientists will probably take their money and leave. In the not too distant future, there might be a lot of top research talent available for smaller biotechnology companies to pick up.

Wednesday, March 25, 2009

Allergan: Going, Going...

Allergan (AGN) stock spiked recently on speculation that GlaxoSmithKline (GSK) would acquire the specialty pharmaceuticals company. I've thought for a long time that GSK would make a play for AGN. Allergan's valuation is significantly lower than before given the current market conditions. Ophthalmology assets have been very popular, e.g. Alcon and AMO acquisitions. The companies already have a strategic partnership. Assuming that GSK has even made an offer for AGN, the big question is price - AGN CEO, David Pyott, has always maintained that he's not interested in selling the company, but everyone has a price. Price will greatly depend on whether GSK believes Botox for migraine will receive FDA approval. Botox would be a great addition to GSK's migraine franchise. Botox for overactive bladder, if it gets approved, would benefit GSK's urology franchise. If GSK believes that the economy will recover soon and that AGN's aesthetic business will eventually rebound, the timing may be right for an acquisition. I could be wrong, but I don't believe there are any other potential suitors for AGN, so I don't think there will be any competitive bids. J&J already bought Mentor, Novartis acquired Alcon, Abbott purchased AMO, and Pfizer is busy with Wyeth. Again, it all comes down to price. Wachovia analyst, Larry Biegelsen, thinks that Allergan shares are worth $60 or more. I wonder if AGN's board thinks the same; they could easily reject GSK's offer if it's not high enough.

Disclaimer: I own Allergan stock; I have owned the stock for a number of years. Investment decisions based on potential acquisitions are highly speculative and risky. There is absolutely no evidence that GSK has made an offer to acquire AGN.

Disclaimer: I own Allergan stock; I have owned the stock for a number of years. Investment decisions based on potential acquisitions are highly speculative and risky. There is absolutely no evidence that GSK has made an offer to acquire AGN.

Tuesday, March 24, 2009

Strategic Investors Can Be White Knights

Despite the current financing crisis, strategic investors are still doing deals. Eli Lilly and Amylin recently entered into a licensing agreement for the rights to Altea Therapeutics' exenatide transdermal patch technology. The deal includes an upfront licensing payment, regulatory and sales milestones of up to $46 million, and royalties. Lilly and Amylin also made an equity investment in Altea. My friends in business development at biopharma and medical device companies have said that they are still looking to do deals, but they also know that valuations are lower and it's a buyers market. No point in rushing into a deal when they know that a startup doesn't have too many alternatives to financing.

Tuesday, March 17, 2009

With Adversity Comes Opportunity

As mentioned in a previous post, the financing environment for pre-revenue life science companies is challenging. The IPO window is closed, and venture capitalists have become more stingy about deploying capital. Unfortunately, some start-ups will be unable to find financing and will fold. According to BIO, ten biotech companies have already gone bankrupt since November of last year. About a third of publicly traded biotech firms have less than 6 months of cash on their balance sheets. I hate to encourage taking advantage of others misfortune, but for those who survive and have cash, opportunities to pick up valuable assets for very little may abound. Keep an eye on bankruptcy filings. Unfortunately, the DowJones Bankruptcy Review requires a subscription, but the WSJ Bankruptcy Beat might be viable a free alternative.

Tuesday, March 10, 2009

The Impact of Big Pharma Consolidation on VC

M&A deal flow has generally declined given the current economic conditions, but not so for the drug industry. Analysts have been predicting for a while that the drug industry would consolidate; big pharma companies are cash-rich, have shrinking pipelines, and face an oncoming "generic" cliff. Merck recently announced a merger with Schering-Plough -- the deal may be complicated by J&J. Earlier this year, Pfizer announced its plans to acquire Wyeth. And the Roche acquisition of Genentech looks like it may finally come to a close. With all of these mega-deals occurring, some VC's have raised concerns about whether any smaller, venture-baked deals will take place. Integration of large companies is painful, but I doubt that good business development people will let valuable assets fall into the hands of competitors just because their company is busy with a merger.

Sunday, March 8, 2009

Where's the R&D?

Traditionally, R&D has been considered a core asset for drug companies, both large and small. But commercial drug companies now appear to be reconsidering the value of their R&D organizations. Both Sanofi-Aventis and Valeant Pharmaceuticals recently announced cutting their R&D budgets in half. The moves are not entirely surprising. R&D productivity has been declining over the past several years, and internally developed compounds have a lower rate of success when compared to licensed compounds (Leerink Swann, March 4, 2009). As the risks and costs of drug development increase, more drug companies will likely reduce internal programs and essentially "outsource" R&D, so that management can focus resources on commercial development. One thing is for certain: look for licensing/partnering activity to expand significantly.

Monday, March 2, 2009

VC Financing in the New World

It should be no surprise that the current financial crisis is negatively impacting VC financing. Limited partners are having problems making capital calls, and IPOs are no longer an option for an exit. Cooley Godward Kronish LLP recently released its report on venture capital financing terms for 2008. As expected, valuations significantly deteriorated in Q4. How does the new financing environment impact life sciences investments? According to VentureSource, investment in U.S. health care companies decreased by 42% in Q4 compared to the same quarter in 2007. An article in the February edition of Nature Biotechnology summarizes some of the negative consequences, especially for early-stage health care startups. As VCs become more risk-averse and as valuations come down, later-stage investments will probably be more favored, and terms will be more onerous for the entrepreneurs.

Thursday, February 26, 2009

The Venture Capitalist Is Dead! Long Live the Venture Capitalist!

I recently attended the Medical Device Growth Conference in San Francisco. Not surprisingly, the mood was pretty grim given the current financial environment. One of the discussion topics was whether the VC business model was dead. Alan Patricof from Greycroft Partners recently wrote an article in the NY Times about the subject. With fewer exit opportunities and less funding, the VC industry will likely contract. I doubt many people will argue that a number of VC funds will not survive the current financial crisis, but is the entire industry dead? Phil Young, from U.S. Venture Partners, was a member of a panel and reminded everyone that he's been hearing that the model was dead ever since he started working in venture capital over 20 year ago. As the financial landscape evolves, the VC industry will likely adjust with the changing environment as it always has.

Subscribe to:

Posts (Atom)